Business Impact

At a Time of Plenty, Some Technologies Are Shut Out

New funding methods claim to democratize investment in innovation, but important technologies still struggle.

Today there are more ways to fund a new company than ever—from crowdfunding platforms to early-stage angel investors, tech incubators that nurture ideas in management boot camps, wealthy family foundations, corporate venture funds, and record levels of venture capital.

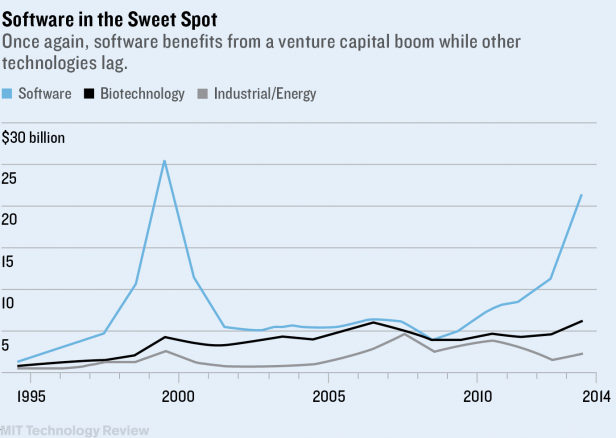

On crowdfunding platforms, where entrepreneurs are now raising billions of dollars a year, the big winners are companies making some kind of object that consumers can envision buying and using themselves. Among venture capital investments, software is reaping the lion’s share: $21.5 billion in 2014, or 42 percent of all dollars invested, compared with $6 billion for biotechnology and $2.4 billion for industrial and energy companies, according to data from an annual study by PricewaterhouseCoopers and the National Venture Capital Association.

This limited focus is driving up the valuation of certain kinds of companies and creating an investing bubble. But an even more important issue—the central question in this Business Report—is whether the mechanisms for funding innovation today can nourish a broad range of technologies: not just car-sharing services like Uber, but valuable technologies for making energy cleaner, reducing poverty, and improving health care.

“The best ideas don’t always get financed,” says Harvard Business School professor Ramana Nanda, an expert in entrepreneurship funding.

Among the areas suffering from insufficient investment, according to a recent report by a committee of MIT professors: medical research into Alzheimer’s and infectious diseases, cybersecurity for non-defense systems, agricultural R&D that could help address the world’s soaring need for food, and even areas of next-generation computing.

Capital-intensive industries are particularly ill-suited to today’s methods of funding. For example, it can take years and hundreds of millions of dollars to determine whether innovations in large-scale energy production can work, because they require the construction of a factory or some other large facility. Though venture investors showed interest in energy startups for a brief period in the late 2000s, that window of opportunity has largely closed, leaving the companies scrambling to find new options.

When Aaron Fyke founded his company Energy Cache in 2009, it was a good time for green-energy startups. The company, which was developing a mechanical battery to inexpensively store energy generated by wind turbines and solar power, attracted early seed investing from the tech incubator Idealab and others, and it used that to build a prototype. But when Energy Cache went back to investors several years later looking for $20 million to fund two more rounds of development before the product could get to market, it was hard to find investors interested in investing in this type of energy technology.

Now raising money for a new company, Edisun, with a faster track to commercialization and a lower cost to develop its technology, Fyke says investors—including traditional venture capitalists, corporate VC arms, and wealthy individuals—have been much more enthusiastic.

Given the lack of big money, entrepreneurs like Fyke have had little choice but to refocus on low-capital technologies that use off-the-shelf components, but while that makes sense for them, it still leaves a question: how do we fund the high-capital technologies that we will also need?

For this group, funding has to be found beyond Silicon Valley venture capital firms—perhaps led by governments or by investors with a longer time horizon, like family foundations or corporate venture funds. GE Ventures, for instance, invests $200 million a year in startups in such fields as software, advanced manufacturing, energy, and health care. It has stakes in companies including Rethink Robotics and Airware, which makes drone software. “For the most part what we are investing in, we hope to be customers of,” says senior managing director Karen Kerr.

For medical-device makers—which, like energy companies, often draw little interest from VCs—crowdfunding has strategic advantages. Scanadu, the maker of a small device packed with sensors that can measure temperature, heart rate, blood pressure, and other bodily signals, has smartly use its fund-raising to prove market interest. By raising $1.6 million on Indiegogo, the company got 7,000 backers eager to test its prototypes. That provided valuable data to show regulators reviewing the device and helped persuade later-round venture capital funders that there is a market for Scanadu’s products.

Now four years old, the company has $49.7 million in backing—including funds from two strategic Chinese backers, the Internet giant Tencent and the investment group Fosun, which has a large health business. It has begun thinking of rolling out in China after the U.S.

The dominance of venture capital in the innovation-funding environment is not just a U.S. phenomenon. China, once exclusively a bastion of government-funded research, is now the second-largest VC market, behind the United States. Companies in China collected 18 percent of global VC investment in 2014, or about $15.6 billion, compared with $4.8 billion the year before, according to data compiled by the global accounting firm EY. India’s share has been climbing too, with $5.2 billion invested in 2014—more than double the 2013 total of $1.9 billion.

Yet in this increasingly global funding picture, certain innovations are still struggling: potential breakthroughs in energy production and medicine, among others, that take too much money and time to develop. A better financing system, says Harvard’s Nanda, would support a sort of Darwinian evolution of technology. “Each new technology is like a mutation,” he says. “Most will end up failing. A few will be an incredible success. We want to develop financial systems that will encourage experimentation and a high rate of new variations and then be quick at shutting down those that don’t work.”