Business Impact

Modern Money Compared

Payment apps are all the rage. But how well do they work?

Picture this: You’re at a restaurant table surrounded by friends and acquaintances, and the end of the night approaches. The waiter picks up his check holder to find three different credit cards, accompanied by detailed instructions about which ones should be charged how much. He informs you that the restaurant does not accept cards. Since you are the one person who always has cash, you reluctantly pay the entire bill. You doubt anyone will pay you back in a timely fashion, if at all.

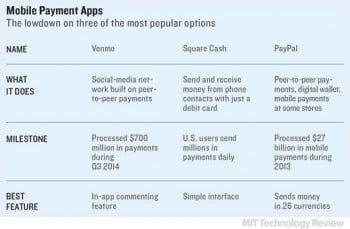

This is the type of scenario mobile payment apps, which allow you to send money digitally to a friend’s account, were made for. Apps from Venmo, PayPal, and Square have spread quickly through word of mouth to become a staple in many Americans’ lives. Venmo, a free peer-to-peer payment app attached to a social-media stream, is now processing $700 million in transactions per quarter.

But are these apps any more useful than cash, checks, and the old-fashioned IOU? The short answer is yes.

Though some of apps offer a variety of services, I focused on the central tasks of sending and receiving money. I downloaded and tested the apps in November and December 2014, linking each one to a debit card and, when necessary, my bank account and routing number. I tested each app by exchanging funds with people I already knew. All seemed secure, either requiring you to unlock the app with a PIN or giving you the option to add that layer of security.

App: Square Cash

Payment methods: U.S.-based MasterCard and Visa debit cards. No credit cards.

Fees and limits: Free. The first time you surpass the initial spending limit of $250 per week, the transfers become more complicated, requiring personal information like your birth date or the last four digits of your Social Security number. After you enter that information, the weekly spending limit is $2,500. You can also receive up to $1,000 per month simply by signing up for the app, but if you want to receive more than that, you must give more personal details.

Currencies accepted: U.S. dollars

Strong suit: Getting paid quickly with minimal hassle

I found Square Cash to be the easiest app for sending money to the bank account of someone who needs it right away. It has a sparse, utilitarian design. After typing in my debit card details, I could immediately send money to, or receive money from, anyone whose phone had the app installed. The screen looks like a calculator. There’s a big field that flashes “$0” at the top until you punch in the amount you want to send. After that, you have two options. You can hit “Request,” which scours your phone’s contact list for the person you want to tell that you need that amount. Or you can press “Send,” which sends that amount almost immediately to the desired recipient’s bank account. You can add a memo, and the app notifies you when the money is deposited into your bank account or your friend’s account. Unlike other apps tested, Square Cash does not require you to add your bank account number to receive money, something that can be a hassle when you’re on the go. You can find other users in the area via Bluetooth, making it easier to pay back people who are not yet on your contact list.

There’s also Snapcash, a version connected to the popular photo-sharing app Snapchat. The interface is different, and I found it harder to use.

Many of Square Cash’s security features are behind the scenes, which allows for an easy payment experience. An optional feature requires users to enter their card’s CVV number each time they send money, which can prevent unauthorized use by a thief who gets hold of a user’s phone. Information is encrypted and stored on Square servers using tokenization, adding to the system’s security.

Would I use it again?

Yes. I probably would not use the Snapcash version again, though.

App: Venmo

Payment methods: Major debit and credit cards

Fees and limits: Free to send money from your Venmo balance, made up of the money people send you through the app. There’s a fee of 3 percent for payment from a credit card or lesser-known debit card. Receiving money is always free. The sending limit is $2,999.99 per week, but identifying information like your zip code, or Facebook account details, is required after $300.

Currencies accepted: U.S. dollars

Strong suit: Fun

Since launching more than two years ago, Venmo has become popular with young people as a social network that tells the world when people pay each other and why. One friend accurately divulged that she sent me a dollar for “using technology,” but the public feed shows memos running from the tame—“Kanye West fan club enrollment fee”—to the unprintable. Venmo defaults to making these updates completely public, but one can adjust the settings to make transactions private or visible only to friends. Like Square, Venmo has a function that allows you to discover other people using the app nearby.

The thought of telling other people what I was spending money on was uncomfortable for me at first. It seemed crass. I put this judgment on hold for a while, however, to see how the app worked. I found it slightly slower to set up than Square Cash but relatively easy to use after that initial housekeeping.

You can send and receive payments about as quickly with Venmo as you can with Square. However, the money is immediately available only as a balance on your app: you can use that to pay other Venmo users, but not for much else.

With Square, by contrast, that money shows up in your bank account. To get money into my bank account with Venmo, I had to dig up and enter the account and routing information, and then wait a day for Venmo to post two small sums to my debit card.

I didn’t realize at first that you could leave a balance on Venmo to pay other people without linking your bank account. I found that process inconvenient because I was set on getting money into my account. People who use Venmo often may not see this as an issue. Customers of Chase, Wells Fargo, Bank of America, and Citibank can link their accounts more simply.

Venmo gives users the option of requiring authentication, such as a PIN, to open the app on their phone. Other than that, the main security feature I encountered when testing the app was the process to verify my bank account. Behind the scenes, Venmo encrypts and stores users’ information on secure servers, which are protected by a firewall and not directly connected to the Internet.

Would I use it again?

Probably. You can easily comment on transactions to thank a person for the money sent or share an inside joke about the event where the transfer took place. With Square, I found myself texting people separately to thank them for sending me money. Honestly, though, I am less likely to keep using Venmo. While the app works great for sending a few bucks quickly, the time one could waste digesting the status updates could easily eat up the time saved not going to the ATM.

And the rest

Google Wallet and PayPal also have mobile apps, but I didn’t find them as useful. Though PayPal has strong security and was the only app that could move money between 26 different currencies (for a fee of 0.5 percent to 2 percent with a U.S. bank account or PayPal balance), others were better at domestic transfers. Unlike Venmo or Square, PayPal offers no way to use a debit card to send people money without incurring a fee.

Balances on Google Wallet can be used at some stores, a plus, but overall I found the app less useful. To claim even a small transfer, you must enter extensive personal verifying information.