Business Impact

Manufacturing in the Balance

Inexpensive labor has defined the last decade in manufacturing. The future may belong to technology.

When General Electric expanded manufacturing of home heaters and refrigerators at its facility in Kentucky last year, the reasons included big wage concessions the company had won from local workers and the advantages of being closer to its U.S. customers. But writing in the Harvard Business Review last March, CEO Jeffrey Immelt explained that one of the biggest factors in GE’s decision to bring back manufacturing from China and South Korea was the desire to keep appliance designers near its manufacturing and engineers.

“At a time when speed to market is everything, separating design and development from manufacturing didn’t make sense,” Immelt wrote. Now, someone who has an idea for a dishwasher that has fewer parts and weighs less can actually try to build it. These designs won’t be so quick to end up in knockoff products built by GE’s suppliers, either. “Outsourcing based only on labor costs is yesterday’s model,” Immelt said.

At the turn of this century, manufacturing wages in southern China were 58 cents an hour, just 3 percent of U.S. levels. GE and many other manufacturers rushed to take advantage of so-called labor arbitrage by moving manufacturing overseas. In 2004, the Boston Consulting Group told clients the choice wasn’t whether to go offshore but “how fast.”

The strategy adopted by many multinational conglomerates, whether based in the U.S. or in Europe, was simple: substitute inexpensive labor for capital. Why invest in a machine to assemble iPhones when Chinese companies could throw half a million workers at the problem? The Internet, telephones, and affordable air travel and sea shipping made it easier than ever to coördinate labor from far away.

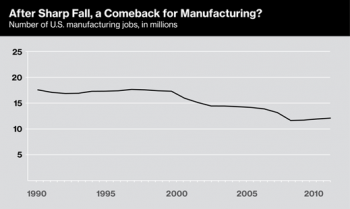

Partly as a result, the U.S. lost about six million manufacturing jobs—33 percent of the total—between 2000 and 2010, and China has overtaken the U.S. as the world’s largest producer of manufactured goods. But the impact extends beyond macroeconomic statistics.

In Producing Prosperity, a book published this year, Harvard Business School professors Gary Pisano and Willy Shih call offshoring of manufacturing a “grand experiment in de-industrialization.” They and others now believe that the consequences have been unfortunate because innovation is hard to separate from manufacturing in technologically advanced areas. Without understanding the details of production, you can’t really design the most competitive products. Eventually, what Immelt calls “core competencies”—such as product design and understanding of materials—are put at risk (see “Can We Build Tomorrow’s Breakthroughs?”).

Lately, however, economic trends have been turning. Wages in China’s southern cities have been rising fast and may soon reach $6 an hour, about what they are in Mexico. Boston Consulting Group—the same consulting firm that told clients to run, not walk, overseas—now says it’s time to “reassess” China and estimates that for some products, that country’s overall cost advantage could disappear by 2015.

The vanishing comparative advantage of Asian cheap labor isn’t the only reason for companies to question offshore manufacturing. Natural catastrophes can occur anywhere, but the risks of long supply lines became apparent in 2011, when the Japanese earthquake and tsunami interrupted shipments of computer chips and floods in Thailand left disk-drive factories under 10 feet of water. Meanwhile, higher oil prices have quietly raised the cost of shipping goods. And a bonanza of cheap natural gas has made the U.S. a relatively cheap place to manufacture many basic chemicals and is providing industries with an inexpensive source of power.

The kind of manufacturing in which labor costs are most important isn’t ever coming back from low-wage countries (assembling five million iPhones for a product launch can still only be done in China), but the recent economic shifts are giving companies a chance to adjust course. One major line of thinking, the one most vocally endorsed by the White House, is that the U.S. should focus its efforts on advances in the technology of manufacturing itself—the set of new ideas, factory innovations, and processes that are also the focus of this month’s MIT Technology Review business report.

The U.S. holds advantages in many advanced technologies, such as simulation and digital design, the use of “big data,” and nanotechnology. All of these can play a valuable role in creating innovative new manufacturing processes (and not just products). Andrew McAfee, a researcher at MIT’s Sloan School of Business, says it’s also hard to ignore coming changes like robots in warehouses, trucks that drive themselves, and additive manufacturing technologies that can create a complex airplane part for the price of a simple one. The greater the capital investment in automation, the less labor costs may matter.

Because manufacturing is so heterogeneous, no single technology can define its future direction. But for advanced economies like the U.S., the questions don’t change. Says McAfee: “If labor is not the differentiating factor, you need to ask, ‘What can be?’”

Advertisement