How the iPhone 5 Will Yet Again Fail to Eliminate Credit Cards

Near Field Communication technology has been in phones since 2006, and there’s a reason it has yet to take off.

It’s been a while since the rumors flew that the next iPhone would have Near Field Communication built in. The technology allows you to touch a phone to a receiver/transmitter, and the two have secure electronic intercourse and a millisecond later out pops a transaction. That’s the idea, anyway.

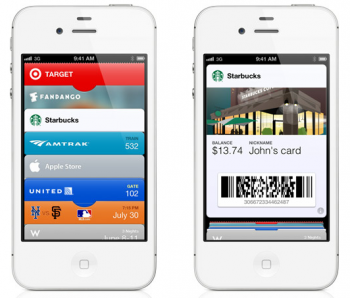

NFC is used in Google’s Wallet, which has yet to gain traction in part because it’s compatible with exactly one credit card. Many pundits are excited about the prospect of an iPhone with NFC technology combined with the already-announced Passbook app that will be part of iOS 6, Apple’s next operating system for the iPhone and related devices. Passbook will store documents on the phone, but can also be used for transactions like buying a coffee at Starbucks. The mechanism of exchange in that case is a QR code, however.

NFC has been in phones since 2006, so why aren’t we all using digital wallets by now? As futurist Scott Smith points out on Twitter, one of the problems is that “banks and operators would want a pound of digital flesh somewhere.” Indeed, even as operators like Square and Stripe try to make an end-run around banks, they remain inherently dependent on them. It’s a safe bet that Visa and Mastercard aren’t about to cede an inch of the incredibly lucrative trade in usurious rates on easy credit they’ve built up over the years.

NFC payments are common in Japan and Korea, but in both countries, monopolies in banking and cell carriers were instrumental in making it happen, says Smith.

So what’s Apple planning to do with NFC in its phones? The technology could be used for file transfers, for one. (Before they switched strategies, the founders of business card app CardCloud planned to use NFC to allow transfers of digital cards.) Beyond that, the use cases just aren’t that compelling. A recent, breathless Businessweek piece on NFC outlined applications like scanning your spice cabinet for recipe ideas and using the technology to exchange information at large events. There are plenty of interesting edge cases for the technology, but it’s hard to see any of them being compelling enough for an Apple announcement.

There’s also, of course, the possibility that Apple will allow payments via NFC in the iPhone 5 after all. But it remains to be seen whether the number of payment options will increase. The company is notoriously finnicky about empowering players in the value chain other than itself. Absent a sea change in banks’ apparent reluctance to make NFC a real standard, it’s hard to imagine adoption of “digital wallets” hitting an inflection point in the US any time soon.