Business Impact

How Mobile Phones Jump-Start Developing Economies

Ubiquitous handsets introduce mobile payments to those who lack bank accounts.

As one of the fastest-spreading technologies in history, the mobile phone has been transformative for the billions of people in the developing world who never had a landline or an Internet connection. One of the most unexpected benefits is its ability to deliver banking services.

Veronica Suarez, like some 2.5 billion other adults on the planet, has no bank account of her own. Suarez and her husband run a small grocery store in Quito, Ecuador, a city of about 1.4 million people on a plateau ringed with dormant volcanoes. In the past, she would often spend half a day traveling to pay bills in cash. But since June, she has been testing a mobile banking service called Mony, which is run by the Panama-based startup YellowPepper Holding. Now she can simply type out text messages that zap payments to the phones of the delivery men who bring cases of Coca-Cola and boxes of vegetable oil to her shop. That could enable her to save travel time, reduce the risk of getting robbed, and run her business more efficiently.

“It works pretty well,” says Suarez, whose store is one of 52 mom-and-pop shops in Ecuador taking part in the tests. “But sometimes I am $50 short to pay the delivery man. It would be better if they loaned money, too.”

Soon, they might. Worldwide, dozens of companies are introducing mobile wallets that store money in cell phones instead of bank accounts. Such schemes help the vast ranks of the “unbanked”—those huddled masses who yearn to easily send funds to distant family members, pay bills, or even take out small loans, but don’t have access to financial services. “The mobile wallet can be transformational,” says YellowPepper’s founder and president, Serge Elkiner, who was in Ecuador in November demonstrating his system to officials from neighboring Colombia. “We have the chance to bring hundreds of millions into the banking system.”

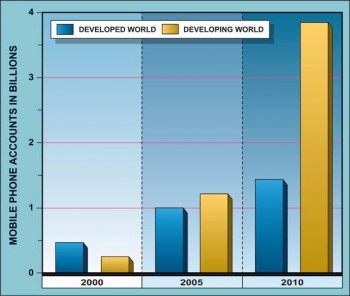

Entrepreneurs say mobile wallets are feasible thanks to the rapid expansion of cell-phone use in poorer regions of the world. In the past five years, operators have added more than two billion mobile accounts in developing and poor nations, according to data from the International Telecommunication Union. That compares to 435 million new accounts in wealthy nations (see chart).

As a result, even in poor regions without clean water or electricity, most adults are now connected. “In pretty much any developing country, in any rural area, you can get the four Cs: Coca-Cola, cigarettes, condoms, and cell phones,” says Robert Katz, an associate with the Acumen Fund, a nonprofit that invests in companies trying to address poverty. “The cell-phone companies have been successful in creating ubiquity, so the challenge for the next generation of startup companies and entrepreneurs is leveraging that installed base to deliver real economic and social value to the poor.”

There’s no shortage of ideas for how to do that. One company in India is offering basic medical diagnoses over the phone to people who live far from a doctor; patients can pay with phone credits. Others are trying to deliver market information to farmers or fishermen, so they can take their goods to the places where they are in demand.

In Ecuador, the Mony service is filling a real need, says Elkiner. According to the consulting firm Bankable Frontier Associates, more than 75 percent of Ecuadorians have a cell phone but only 35 percent have a bank account, about average for poor and developing nations. To open a conventional bank account in Ecuador, you need several hundred dollars and proof of address—two things many Ecuadorians don’t have. To sign up for a YellowPepper mobile account, all that’s needed is an ID, a $5 deposit, and a cell phone. The service is slated for launch in 2011 in partnership with mobile-phone company Porta and a local bank.

Source: International Telecommunications Union

YellowPepper will charge 49 cents per cash transfer. Even though that’s a 1 percent charge on a transfer of $50, Elkiner says he thinks the price is fair. It’s about a third the cost of traditional money transfers, and he adds, “If no one does this you’ll be stuck in the Stone Age again, taking your donkey and paying your bill, and it’s going to take all day.” In October, YellowPepper received a vote of confidence from the International Finance Corporation, an arm of the World Bank, which invested $3 million in the company.

Entrepreneurs targeting the poor are inspired by the notion of doing well by doing good. The business model was popularized by University of Michigan business professor C. K. Prahalad; his 2005 book The Fortune at the Bottom of the Pyramid surveyed early examples of companies making profits while meeting the basic needs of the world’s four billion “microconsumers,” who get by on less—often far less—than $20 a day.

Until recently, the poor simply weren’t viewed as real consumers. But as Prahalad points out, the rapid adoption of mobile phones has shattered preconceptions about what the poor want, and what they can afford to buy. Now many socially minded entrepreneurs think mobile wallets could become the next poverty-killer app. According to the GSMA, an industry group for the mobile communications business, there are now 79 mobile money systems globally, mostly in Africa and Asia. Two-thirds of them have been launched since 2009.

To date, the most successful example is M-Pesa, which Vodafone launched in Kenya in 2007. A little over three years later, the service has 13.5 million users, who are expected to send 20 percent of the country’s GDP through the system this year. “We proved at Vodafone that if you get the proposition right, the scale-up is massive,” says Nick Hughes, M-Pesa’s inventor. The ability to safely save even small amounts can help the poor build assets. One study of a mobile wallet system in the Philippines found that users stored an average of $31, or about a quarter of their family savings, on their phones.

But Hughes says one major obstacle remains: mobile operators themselves. Busy cutting costs and chasing new voice subscribers (about half of African adults still don’t have a mobile phone), operators still consider mobile money a fringe idea. “The opportunities to reach the poor are still beyond the comfort zone of the big companies,” Hughes says.

That’s why last year he left Vodafone to start a venture fund, Signal Point Partners, whose motto is “Scalable services meeting fundamental needs.” Hughes is now betting his own money (and that of investors) on new businesses like a telephone-based medical-advice service in Bangladesh and a mobile borrowing scheme in Kenya. “We have a technology base that is mobile, low cost, and lets you think about something designed for mass population,” he says. “But it starts with something simple, like sending money or calling a doctor.”