Convergence Is King

Rupert Murdoch addresses the Wall Street Journal newsroom after acquiring the paper in 2007.

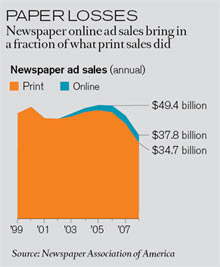

It’s not hard to name the biggest losers in today’s media landscape: newspapers. In 2009, more than 130 U.S. newspapers either closed or moved to online-only publication, typically with skeleton staffs. The big-city daily papers that once defined American journalism have seen their business model collapse as Internet-based competitors commodified news and slashed the cost of advertising.

Newspapers have no problem attracting readers online; the Newspaper Association of America reports that its members’ websites draw 74 million unique visitors per month. The problem is figuring out how to make money. Many publishers, of course, would like to start charging for content. But publishers “aren’t talking about what kind of [additional] value they are going to give their customers or how they are going to use technology in an innovative way,” says Robert Picard, a professor of media economics at Jonkoping University in Sweden and the editor of the Journal of Media Business Studies.

Dow Jones has been able to charge online for the Wall Street Journal, because its specialized content is not easily found elsewhere. Similarly, Bloomberg manages to charge premium prices for business news and information. This suggests an approach for struggling newspapers: by developing niche coverage, such as in-depth reporting on a sports team or a particular industry, they can offer content that is hard to duplicate. Online, such content may also find a wider audience than the local readers that newspapers traditionally served. Earlier attempts at charging for such products failed, probably because of the high prices publishers set. Last September, in a lower-priced experiment with this kind of strategy, the Minneapolis Star Tribune launched a premium website centered on the Vikings football team; three months’ access costs $5.95.

The key technical characteristic of what works is the ability to facilitate consumers’ desire to read, watch, or listen to any content they want, anywhere, anytime. For print media, that makes it attractive to sell subscriptions on devices such as Amazon’s Kindle and Barnes and Noble’s Nook; 2.6 million e-readers are expected to be sold in the United States in 2010, more than twice as many as in 2009.

Beyond print, the many companies vying to put video on television screens are drawing investors’ interest. Netflix, for example, has partnered with Roku to provide a set-top box for televisions that streams movies from Netflix’s online catalogue; Microsoft and Sony are pushing their game consoles as on-demand media players; and Intel and Yahoo are collaborating on built-in software and chipsets that will enable televisions to run interactive applications.

Who is the king of new media? Apple. Despite the global economic meltdown, Apple has converted consumers’ appetite for convergence into the biggest profits in the company’s history, selling more than 33 million iPhones since the device’s introduction in 2007–21 million in the 2009 fiscal year alone. In the new-media gold rush, it is selling the picks and shovels: its media business model, much like Google’s, is dedicated to making it easier for users to enjoy other people’s content. The iPhone represents just the latest advance in Apple’s convergence strategy, which dates back to the 2001 launch of the iPod music player and 2003 launch of the iTunes music store. Defying the conventional wisdom that people won’t pay for anything they can get online free, Apple can “deliver all kinds of content to you in a way that is so seamless that you cannot pass it up,” says James McQuivey, an analyst with Forrester Research. “It’s easier to buy media from iTunes than it is to steal it.”